The method for calculating the final inventory value remains consistent across different accounting approaches. Suppose the number of units from the most recent purchase been lower, say 20 units. We will then have to value 20 units of ending inventory on $4 per unit (most recent purchase cost) and the remaining 3 units on the cost of the second most recent purchase (i.e., $5 per unit).

When to Consider Other Inventory Methods

Second, every time a sale occurs, we need to assign the cost of units sold in the middle column. When a business buys identical inventory units for varying costs over a period of time, it needs to have a consistent basis for valuing the ending inventory and the cost of goods sold. FIFO is recognized and accepted by international financial reporting standards (IFRS) and generally accepted accounting principles (GAAP) in the United States. Compliance with one or both of the accounting practices facilitates easier auditing and financial analysis. FIFO’s widespread acceptance and straightforward logic mean it is supported by the majority of accounting and inventory management software. Mobile inventory management solutions like RFgen can automatically enforce FIFO rules in the warehouse.

- First in, First out inventory method is compliant with IFRS and GAAP, which makes it ideal for companies with global operations or aspirations.

- The first guitar was purchased in January for $40.The second guitar was bought in February for $50.The third guitar was acquired in March for $60.

- All companies are required to use the FIFO method to account for inventory in some jurisdictions but FIFO is a popular standard due to its ease and transparency even where it isn’t mandated.

- It reduces the impact of inflation, assuming that the cost of purchasing newer inventory will be higher than the purchasing cost of older inventory.

- While the FIFO method has many benefits, it’s not without disadvantages.

How Does the FIFO Method Work?

With FIFO, when you calculate the ending inventory value, you’re accounting for the natural flow of inventory throughout your supply chain. This is especially important when inflation is increasing because the most recent inventory would likely cost more than the older inventory. This method dictates that the last item purchased or acquired is the first item out. This results in deflated net income costs and lower ending balances in inventory in inflationary economies compared to FIFO. FIFO assumes that assets with the oldest costs are included in the income statement’s Cost of Goods Sold (COGS).

Simplified Cost Calculation

FIFO (First-In, First-Out) aligns with this principle by serving as a critical framework in inventory management and accounting. It plays a crucial role in various industries, from retail to manufacturing, and helps businesses accurately track their stock movement and financial performance. Three units costing $5 each were purchased earlier, so we need to remove them from the inventory balance first, whereas the remaining seven units are assigned the cost of $4 each. The company makes a physical count at the end of each accounting period to find the number of units in ending inventory. The company then applies first-in, first-out (FIFO) method to compute the cost of ending inventory. Under first-in, first-out (FIFO) method, the costs are chronologically charged to cost of goods sold (COGS) i.e., the first costs incurred are first costs charged to cost of goods sold (COGS).

How Is the FIFO Method Calculated?

It reduces the impact of inflation, assuming that the cost of purchasing newer inventory will be higher than the purchasing cost of older inventory. Alternative methods include LIFO, Weighted Average Cost, Specific Identification, and Standard Costing. LIFO assumes the newest inventory is sold first, resulting 5000 freelancer auditor jobs in united states 257 new in a higher cost of goods sold during inflation. Specific Identification tracks individual item costs, while Standard Costing uses predetermined values while adjusting for variances over time. For example, if you sold 15 units, you would multiply that amount by the cost of your oldest inventory.

What Is FIFO Method: Definition and Guide

FIFO has several advantages, including being straightforward, intuitive, and reflects the real flow of inventory in most business practices. Many companies choose FIFO as their best practice because it’s regulatory-compliant across many jurisdictions. It can be easy to lose track of inventory, so adopt a practice of recording each order the day it arrives. This makes it easier to accurately account for your inventory and maintain proper FIFO calculations. Some companies choose the LIFO method because the lower net income typically leads to lower income taxes. However, it is more difficult to calculate and may not be compliant under certain jurisdictions.

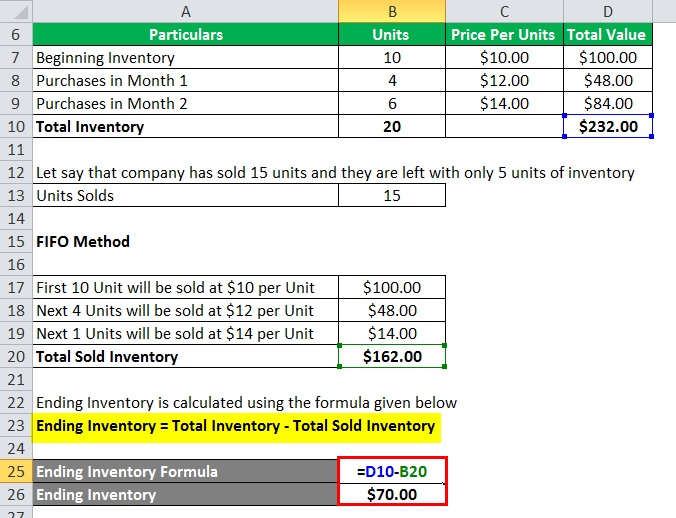

In the FIFO Method, the value of ending inventory is based on the cost of the most recent purchases. To find the cost valuation of ending inventory, we need to track the cost of inventory received and assign that cost to the correct issue of inventory according to the FIFO assumption. On 1 January, Bill placed his first order to purchase 10 toasters from a wholesaler at the cost of $5 each. Certain chemicals, when left to sit, risk degrading, becoming unstable, or forming hazardous byproducts—all of which compromise product quality and human safety. Therefore, FIFO helps maintain compliance with health, safety, and environmental regulations.

Powerful mobile inventory solutions like RFgen can help your enterprise revolutionize inventory management with automation and barcoding, regardless of what inventory valuation method you use. It helps businesses accurately track inventory costs, calculate profits, and manage stock levels. The FIFO inventory method has significant effects on company financial reports, tax filings, and strategic choices. It can lead to higher reported profits during inflation periods, as older, less expensive inventory is expensed first while newer, potentially pricier items remain in stock. They will handle all of the tedious calculations for you in the background automatically in real-time. This will ensure that your balance sheet will always be up to date with the current cost of your inventory, and your profit and loss (P&L) statement will reflect the most recent COGS and profit numbers.

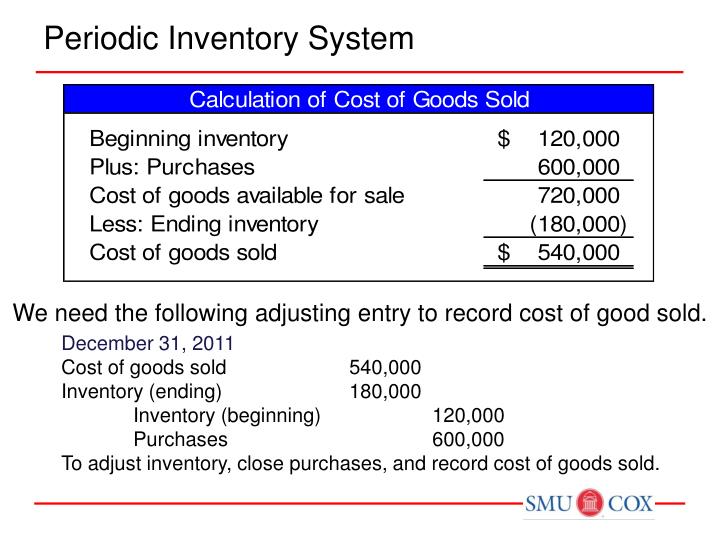

The alternate method of LIFO allows companies to list their most recent costs first in jurisdictions that allow it. Every time a sale or purchase occurs, they are recorded in their respective ledger accounts. However, as we shall see in following sections, inventory is accounted for separately from purchases and sales through a single adjustment at the year end.

To better understand the FIFO inventory method, imagine a gumball machine. The gumballs at the bottom of the machine were likely the first ones added. When you insert a coin and turn the knob, those gumballs at the bottom, which went in first, will be the ones that come out first. The gumballs remaining in the machine at the end of the period—your inventory—are the gumballs that were added last. The goods that you first purchased will be the first ones to go to COGS upon sale.

When calculating inventory and Cost of Goods Sold using LIFO, you use the price of the newest goods in your calculations. Under the LIFO Method, cost of goods sold is calculated using the most recent inventory first and then working our way backwards until the sales order has been filled. Choosing between FIFO and LIFO ultimately comes down to financial strategy. When considering which to use, businesses must weigh strategic considerations like financial reporting, tax implications, and compliance with standards.